TORONTO – October 31, 2022: Urbanation Inc., the leading source of information and analysis on the condominium market since 1981, released its Q3-2022 Condominium Market Survey results today.

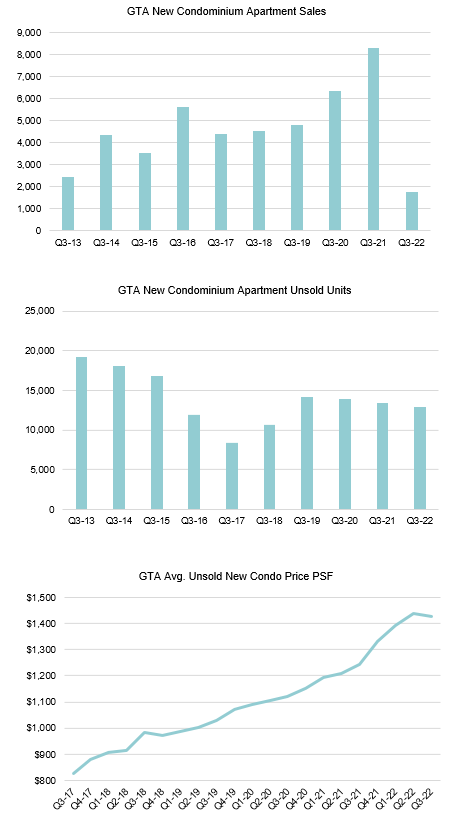

Greater Toronto Area (GTA) new condominium sales totaled 1,748 units in the third quarter, declining 79% from a year ago (8,320 sales). Outside of the initial months of the pandemic in Q2-2020 when 1,585 units sold, this was the lowest quarter for GTA new condo sales since the financial crisis in Q1-2009 (887 sales). A record 189 projects in development reported zero sales during the quarter, a 67% share of total projects with available inventory.

New condominium sales paused as presale purchasers moved to the sidelines amid heightened market uncertainty caused by the rapid increase in interest rates. Facing slow sales and high costs, developers pulled back dramatically on launching new projects. The 2,857 new units launched for presale in Q3-2022 was down 67% from the same period last year (8,627 launches) and 32% below the 10-year average for Q3 (4,181). While there has been a pick up in new launch activity in Q4-2022 with 4,591 units launched so far in October, the market remains on track to see approximately 10,000 units delayed for launch this year. With sales absorption at new launches falling to a more than decade low of 26% in Q3-2022, developers are expected to remain cautious in bringing new pre-construction projects to the market in the near-term.

The slowdown in new condominium sales and presale launches is not expected to negatively impact construction activity until the second half of 2023, as developers will remain active in the next few quarters starting work on the large number of units that launched and sold in previous quarters. The 8,953 new condominiums that started construction in Q3-2022 was up 40% year-over-year and represented a record high for the GTA, pushing the total number of units under construction to a record 96,510.

Despite the record amount of development underway in the GTA, new condominium inventory levels remained low. The 12,943 unsold units available at the end of the quarter was down 3% annually from 13,408 units in Q3-2021 and was 7% below the 10-year average of 13,946 units. The total share of units in development that were pre-sold remained near a record high at 91%.

Low inventories and high development costs continued to put upward pressure on new condominium prices. Projects that launched for presale during Q3-2022 opened with record high average prices of $1,380 psf, based on an average unit size of 642 sf. While the average price for all available units in the market at $1,427 psf in Q3-2022 declined by 1% from the record high in Q2-2022 ($1,440 psf), prices remained 15% higher than a year ago ($1,244 psf). By comparison, the average price for resale condominiums in Q3-2022 declined 5% quarter-over-quarter to $891 psf and 10% from the record high reached in Q1-2022 ($988 psf), creating a record wide discount compared to new condominium prices.

“Condo investors and developers adopted a wait-and-see approach to determine the impact on the market from higher interest rates, resulting in very little sales activity in Q3. While the surge in construction was a positive sign for new supply, it will ultimately be short-lived unless market confidence improves.”

--Shaun Hildebrand, President of Urbanation

Latest Research

April 15, 2025

Slowest Condo Market in Over 30 Years Causing Construction to CollapseJanuary 31, 2025

Ottawa Rental Vacancy Increases as New Completions Continue to GrowJanuary 28, 2025

GTHA Rental Vacancy Highest Since PandemicJanuary 16, 2025

GTHA New Condo Sales in 2024 Were Lowest Since 1996November 1, 2024

Ottawa Rental Construction Falls in Q3 Despite Low Vacancy and Rising RentsOctober 30, 2024

Record Condo Completions Bring Down Rents in Toronto

In The News

April 16, 2025

GTHA Sees Slowest New Condo Sales In Over 30 Years, Construction 'Collapses'April 15, 2025

Toronto and Hamilton-area new condo market sees the slowest quarter in 30 years, says new reportApril 9, 2025

Average asking rents decrease for sixth straight month to $2,119: reportApril 8, 2025

National Average Rent Sees 6th Straight Annual Decline In MarchApril 1, 2025

Landlords are offering free months of rent, complimentary Wi-Fi and Presto cards to attract new tenantsMarch 27, 2025

Storeys: Ontario's Rental Supply Gap Projected To Surpass 200,000 In Next 10 Years