According to Urbanation's latest Q3-2022 Ottawa Rental market Report, rents in Ottawa increased in Q3-2022 to reach a record high.

Below are some highlights of the latest Q3-2022 results:

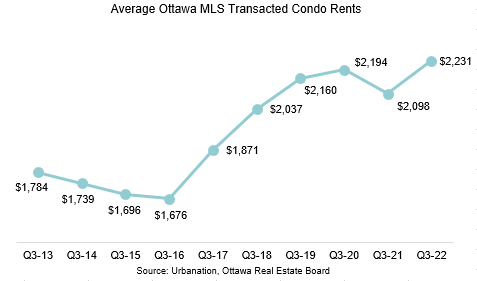

• Condominium rents reached a record high $2,231 ($2.68 psf) in Q3-2022, increasing 3.0% quarter-over-quarter and 6.3% year-over-year.

• Condo rents surpassed their pre-pandemic high for the first time, rising 1.7% over the Q3-2020 average of $2,194.

• The 306 condo units rented last quarter was down slightly (-1%) from a year ago but remained near a record high. Condo rental supply has been held back by a low level of new condo completions in Ottawa.

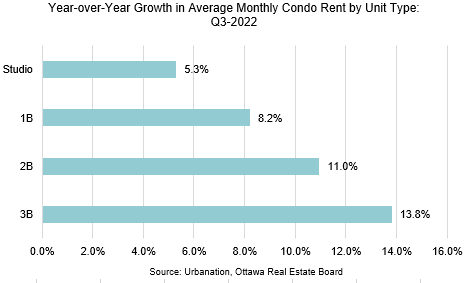

• The fastest annual increases in condo rents were recorded for three-bedroom units at 13.8% and two-bedroom units at 11.0%. Meanwhile, studios recorded the smallest yearly rent increase of 5.3%, and one-bedroom rents were up 8.2%.

• Condo buildings completed since 2020 averaged the highest rents of $3.10 psf.

• The universe of new purpose-built rentals in Ottawa increased to a total of 8,584 units in Q3-2022, rising by 60% (3,202 units) since the end of 2021.

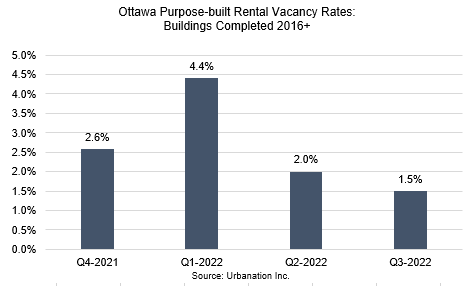

• Despite the strong growth in new rental supply, vacancy rates in stabilized new purpose-built rental projects declined to a pandemic low of 1.5% in Q3-2022.

• The average surveyed rent for available new purpose-built units during Q3-2022 was $2.93 psf ($2,229 for 761 sf), edging down slightly from a high of $2.96 psf surveyed in Q2-2022 mainly due to compositional changes in surveyed units.

• The highest surveyed average rents were found in Sandy Hill/Lowertown at $3.31 psf, followed by The Glebe/Old Ottawa South at $3.26 psf and Downtown at $3.25 psf.

• Compact new purpose-built rentals achieved notable premiums, with studios and one-bedrooms under 500 sf averaging $3.80 psf and two- and three-bedroom units under 800 sf averaging $3.40 psf.

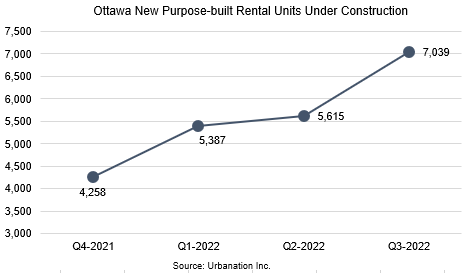

• The inventory of new purpose-built rentals under construction in Ottawa grew to 29 projects totaling 7,039 units, increasing by 2,781 units (+65%) since Q4-2021.

• Longer-term future apartment supply represented by proposed projects that haven’t yet started construction remained at a high of 84,336 units, including 23,253 units identified as purpose-built rentals.

Latest Research

February 9, 2026

GTA Land Transaction Volume Down 20% in 2025February 9, 2026

Rental Vacancy in Ottawa Increased to 3.5% in Q4January 29, 2026

Nearly 10,000 GTHA Rentals Started Contruction in 2025January 21, 2026

New Condo Sales Fall for 4th Year to Lowest Since 1991November 4, 2025

Ottawa Rental Starts Reach Multi-Decade High in Q3October 28, 2025

GTHA Rental Projects Forge Ahead in Q3 Despite Declining Rents

In The News

March 18, 2026

Public-private partnership launches $1.3-billion fund to purchase unsold GTA condosFebruary 9, 2026

Condo crash pushes down Toronto asking rents to $2,500 a month due to ‘sheer volume of supply’February 3, 2026

Toronto is a renter's market — for now — as record glut of condos and apartments collideFebruary 2, 2026

Rental construction surged in Q4-2025January 23, 2026

“No New Condo Completions” In GTHA By Decade’s End: UrbanationJanuary 23, 2026

Toronto and Hamilton-area new condo sales in 2025 were the lowest in 35 years, says Urbanation